DS Smith, down 1.9%, announced that EU antitrust regulators set 10 January 2024 as the deadline for the International Paper-DS Smith deal.

Johnson Matthey, down 9.8%, in its interim results, announced that revenues dropped to £5.63b from £6.53b recorded in the same period of the previous year. Profit before tax widened to £554.0m from £136.0m. Kier Group, down 0.3%, announced that it would design and build a school for a site on the Wolsey Park development, off Rawreth Lane in Rayleigh.

Oracle Power, up 200%, announced that it has received the final batch of assay results from the November 2024 aircore (AC) drilling undertaken during Riversgold Limited's 4th aircore programme at the Northern Zone Intrusive Hosted Gold Project.

Sareum Holdings, up 3.8%, announced that its annual general meeting (AGM) will be held at 10.00 am on 19 December 2024 at 88 Wood Street, London, EC2V 7QR.

Aferian unchanged at 3.3p, today, announced that Bruce Powell has resigned as a Non-Executive Director with immediate effect, following over two years of service on the Board.

Creightons, unchanged at 34.0p, in its interim results, announced that revenues fell to £27.08m from £27.56m recorded in the same period of the previous year. Profit before tax widened to £1.68m from £0.30m.

Dialight, down 22.3%, in its interim results, announced that revenues fell to $90.3m from $91.0m recorded in the same period of the previous year. Loss before tax widened to $20.8m from $6.6m.

Tristel, down 3.4%, in its FY 2024 results, announced that revenue advanced to £41.9m (up 17% from FY 2023). Its earnings per share stood at £0.14 (up from UK£0.094 in FY 2023).

Feedback, down 2.4%, in its commercial update, announced that it has entered into a memorandum of understanding with its partner and an NHS Trust to implement a pilot for a novel 'Neighbourhood Diagnostics Solution' that combines Bleepa with its partner's technology to streamline NHS diagnostic and pathway referrals between primary care, CDCs and secondary care.

Gaming Realms, down 0.5%, announced the appointment of Lauren Bradley as its new Director of Account Management.

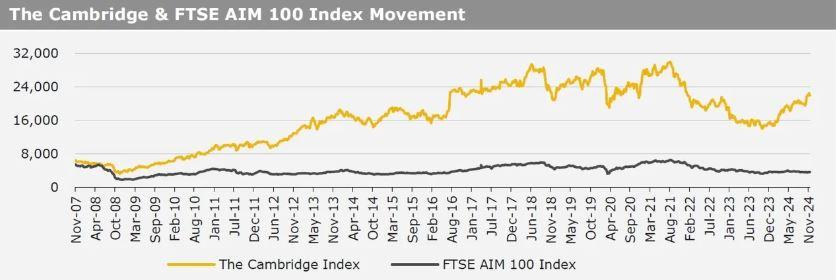

UK markets ended mostly lower last week, as investors await policy decision by the Bank of England. On the data front, the UK BRC shop price index dropped in November. Meanwhile, the UK mortgage approvals increased to the highest level in more than two years in October, as falling interest rates boosted housing market activity. Additionally, the UK’s nationwide housing prices increased at the fastest pace in two years in November. The FTSE 100 index advanced 0.3% to settle at 8,287.3, meanwhile the FTSE AIM 100 index fell 0.1% to close at 3,563.9. Additionally, the FTSE techMARK 100 index lost 1% to end at 6,502.3.

US markets ended higher in the previous week, driven by strong consumer spending. On the macro front, the US annualised gross domestic product grew as expected in 3Q24, amid higher consumer spending, while the nation’s consumer confidence rose to a 16-month high in November. Additionally, the US personal income advanced more than expected in October, while personal spending climbed more than anticipated in October. Moreover, the US pending home sales unexpectedly rose in October, while the nation’s weekly jobless claims unexpectedly fell in the week ended on 22 November 2024. Meanwhile, the US durable goods orders advanced less than expected in October, while the nation’s new home sales dropped to its lowest level in almost two years in October. Separately, the US FOMC minutes indicated that the central bank would move towards gradually lower interest rates given robust US economic growth and fading concerns about the health of the labour market. The DJIA index rose 1.4% to end at 44,910.7, while the NASDAQ index gained 1.1% to close at 19,218.2.