Kier Group, up 7.4%, announced that it has been appointed as its construction partner by Bicester Motion, the 444-acre future mobility estate in Bicester, Oxfordshire to deliver YASA’s new UK HQ at The Ranges, its new name for its innovation quarter.

Feedback, up 30.1%, announced that its Bleepa platform, which facilitates Diagnostic Enhanced Advice and Guidance, is now eligible for reimbursement under the Elective Recovery Fund (ERF), potentially boosting its commercial prospects.

Tristel, up 9.0%, today, in its audited preliminary results for the year ended 30 June 2024, announced that revenues climbed to £41.93m from £36.01m recorded in the previous year. Profit before tax widened to £7.08m from £5.11m.

1Spatial, up 3.9%, in its interim results, announced that revenue rose to £16.25m from £15.54m recorded in the same period of the previous year. Loss before tax narrowed to £0.16m from £0.46m.

Quartix Technologies, up 0.3%, in its trading statement, announced that it renewed its focus on the company's core business and continued to drive strong growth in its annualised recurring revenue (ARR). The company's ARR increased by £3.1m (+11%) in the 12 months from 1 October 2023 to 30 September 2024.

Cambridge Cognition, down 9.7%, announced that it has now received the formal resignation of Dr Stork as a Director of the company and all subsidiary entities of which he was a Director.

Science Group, down 0.6%, today, announced that it has appointed Canaccord Genuity Limited as nominated adviser and joint corporate broker with immediate effect, alongside existing corporate broker Panmure Liberum Limited.

Sareum Holdings, unchanged at 27.0p, today, announced that it has raised a further £1.0m fund from certain investors including the institution that participated in the 11 October 2024 fundraise through a subscription for a total of 4,444,444 new ordinary shares of 1.25p each in the capital of the company at a price of 22.5p per new ordinary share.

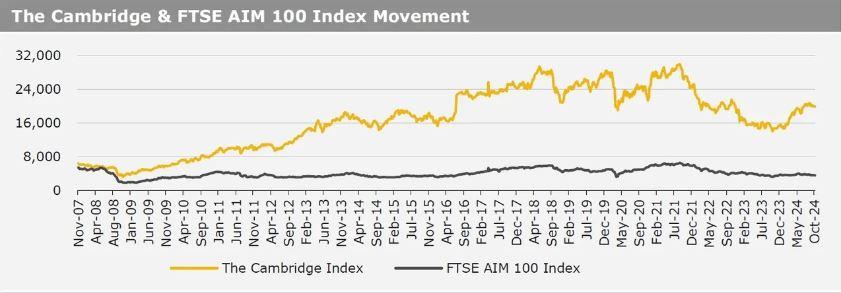

UK markets ended higher last week, amid hopes that the Bank of England (BoE) will cut rates next month. On the data front, the UK ILO unemployment rate unexpectedly fell to three months in August, while the nation’s retail sales unexpectedly grew in September, boosted by higher sales of technology products. Moreover, the UK DCLG house price index advanced in August. Meanwhile, the UK consumer price index rose less than expected in September. The FTSE 100 index advanced 1.3% to settle at 8,358.3, while the FTSE AIM 100 index rose 1.3% to close at 3,604.3. Additionally, the FTSE techMARK 100 index gained 2.1% to end at 6,770.8.

US markets ended higher in the previous week, lifted by gains in technology sector stocks. On the macro front, the US retail sales advanced more than anticipated in September, while the nation’s weekly jobless claims unexpectedly fell in the week ended 11 October 2024. Moreover, the US Philadelphia Fed manufacturing index climbed more than anticipated in October, while the nation’s housing starts fell less than expected in September. Meanwhile, the US industrial production declined more than expected in September, while the nation’s building permits dropped more than anticipated in September. Also, the US NY Empire State manufacturing index unexpectedly dropped in October. The DJIA index rose 1.0% to end at 43,275.9, while the NASDAQ index gained 0.8% to close at 18,489.6.