DS Smith, down 0.7%, announced that its annual report for the year ended 30 April 2022 and the notice of the 2022 annual general meeting (to be held at 12 noon on 6 September 2022 at No.4 Hamilton Place London W1J 7BQ) are published.

Johnson Matthey, up 6.8%, today announced that it is building a gigafactory worth £80m at its existing site in Royston, UK, to scale up the manufacture of hydrogen fuel cell components.

Quixant, up 4.2%, in its trading update, announced that its strong demand across both Gaming and Densitron businesses has continued in the first half of 2022. It expects to release its results for the six months ended 30 June 2022, on 6 September 2022.

Kier Group, up 2.4%, announced that Kier Property acquired two new sites totalling 8.34 acres, a six-acre site in Milton Keynes and a 2.34-acre site in St Albans.

GetBusy, up 1.8%, announced that its 1H2022 revenues climbed £9.1m from £7.5m recorded in the same period previous year.

Tristel, unchanged at 342.5p, in its trading update for the year ended 30 June 2022, announced that it witnessed a rise in the number of patient procedures carried out by hospitals in the second half, across all its geographical market.

CyanConnode, down 6.0%, today, in its trading update, announced that its FY2022 turnover exceeded the market expectation of £9.3m (FY2021: £6.4m).

1Spatial, down 3.1%, announced that it has entered into a five-year contract with the University of Maryland's Center for Advanced Transportation Technology Laboratory.

Xaar, down 1.8%, in its trading update, announced that it has witnessed a strong performance in the first half of the year in line with its expectations.

Oracle Power, down 1.6%, in its trading update for 2Q 2022, announced that during 1Q 2022, it has built on and consolidated developments across its increasingly diversified portfolio of power and natural resources assets.

Quartix Technologies, down 0.9% to 325p. The company, in its trading update, announced that it has witnessed an increase of 26.0% in its new unit subscriptions for 1H 2022.

IQGeo Group, down 0.7%, in its trading update, announced that it expects revenue for 1H 2022 to exceed £8.9m (1H 2021: £6.4m), reflecting growth of 39.0%.

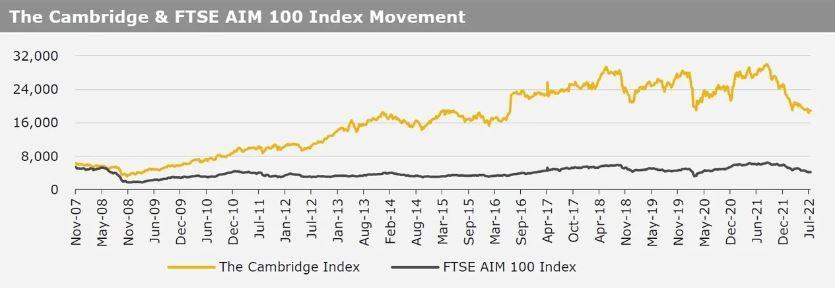

UK markets ended lower last week, amid prospects of aggressive interest rate hikes and a sharp slowdown in the global economy. On the data front, UK’s BRC like-for-like retail sales dropped in June, as inflationary pressures hit consumer spending, while the nation’s house prices advanced to its lowest level since March 2021 in June, as softer demand in the housing sector. Meanwhile, the British economy rebounded in May, amid pent up demand for summer holiday bookings and a large rise in GP appointments. Additionally, UK’s industrial production rose more than expected in May, while the nation’s manufacturing production climbed in the same month. The FTSE 100 index declined 0.5% to settle at 7,159.0, while the FTSE AIM 100 index fell 1.5% to close at 4,197.1. Also, the FTSE techMARK 100 index lost 1.0% to end at 5,771.4.

US markets ended lower in the previous week, amid dismal corporate earnings results from major US banks. On the macro front, the US weekly jobless claims climbed to an 8-month high in the week ended 8 July 2022, indicating a low momentum in labour market, amid rising interest rates and tighter financial conditions. Meanwhile, the US inflation accelerated to a 40-month high in June, amid surging inflation, while the nation’s producer price index climbed more than expected in June, boosted by high energy products prices. Additionally, the US retail sales rebounded in June, suggesting resilient consumer spending, while the US Michigan consumer sentiment unexpectedly advanced in July. The US Fed Beige Book reported that signs of a slowdown have emerged across several parts of US regions in recent weeks, reflecting price increases across the regions remained substantial. The DJIA index fell 0.2% to end at 31,288.3, while the NASDAQ index lost 1.6% to close at 11,452.4.