DS Smith, up 4.9%, announced that its subsidiary, DS Smith Paper Italia has selected ABB to supply a new sectional drive system for a new containerboard machine at DS Smith's paper mill in Lucca, Tuscany.

Hilton Food Group, up 1.6%, in its Q3 trading update, announced that its strong performance in the first half of the year has continued in the third quarter across all three geographical operating regions, with trading in line with the board's expectations.

Kier Group, down 1.7%, announced that it has entered a partnership contract with DroneDeploy, a global leader in enterprise reality capture, to enhance operations across its construction business and projects.

Aferian, up 58.3%, in its trading update, announced that the group has continued to win new business and has received increased sales orders in the second half of the year. As a result, revenue in the second half of the year is expected to be approximately 20% higher than in the first half.

Science Group, up 2.4%, today, in its trading update, announced that its trading performance for FY24 remains on track to deliver another record year of adjusted operating profit in line with expectations.

Cambridge Cognition, up 1.8%, announced that its spin-out company, Monument Therapeutics Limited has received an investment of £1.0m from the Forster Foundation at a post investment valuation of £8.35m.

Oracle Power, unchanged at 0.02p, announced that it has completed the Transmission & Grid Interconnection Study in respect of its proposed 1.3GW hybrid renewable energy power plant in Jhimpir, Sindh Province, Pakistan.

Feedback, down 56.2%, in its final results, announced that revenues climbed to £1.18m from £1.02m recorded in the previous year. Its cash balance as of 31 May 2024 stood at £3.88m (31 May 2023: £7.32m).

CyanConnode Holdings, down 14.7%, in its interim results, announced that revenues fell to £5.63m from £5.78m recorded in the same period of the previous year. Loss before tax narrowed to £2.12m from £2.24m.

Dialight, down 4.9%, announced that its interim results for the period 1 April 2024 to 30 September 2024 will be published on 11 November 2024.

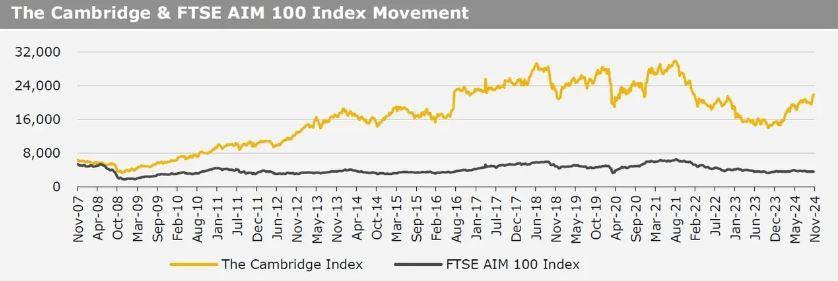

UK markets ended lower last week, as the Bank of England (BoE) indicated future cuts may be more gradual. On the data front, the UK services sector rose at its slowest pace since November 2023 in October, while the nation’s construction PMI dropped more than expected in October. Additionally, the UK BRC like-for-like retail sales rose less than expected in October. Meanwhile, the UK Halifax house prices advanced for a fourth straight month in October. Separately, the Bank of England (BoE) reduced its key interest rates by 25 basis points to 4.75% for the second time since 2020. However, the central bank indicated that future rate cuts were likely to be gradual, citing higher inflation and economic growth after the new government's first budget. The FTSE 100 index declined 1.3% to settle at 8,072.4, while the FTSE AIM 100 index fell 0.7% to close at 3,556.4. Additionally, the FTSE techMARK 100 index lost 0.5% to end at 6,461.5.

US markets ended higher in the previous week, following the US Presidential election 2024 won by Republican Donald Trump and a rate cut by the US Federal Reserve. On the macro front, the US ISM services PMI unexpectedly climbed to a two-year high in October, while the Michigan consumer sentiment index improved more than expected in November. Meanwhile, the US factory orders declined for a second straight month in September, while the nation’s weekly jobless claims rose as expected in the week ended on 01 November 2024. Separately, the US Federal Reserve lowered its benchmark interest rates by 25 basis points to 4.75% for a second consecutive time, as inflation continues to ease. The DJIA index rose 4.6% to end at 43,989, while the NASDAQ index gained 5.7% to close at 19,286.8.