DS Smith, up 0.3%, announced that it has invested €13m in innovative packaging solutions and significant production boost in Romania.

Johnson Matthey, down 3.1%, today, announced the completion of the sale of its Diagnostic Services business in terms of the sale agreement entered into between JM and Sullivan Street Partners for a consideration of £55m.

Kier Group, up 4.0%, announced that it has joined Causeway Technologies’ project aimed at developing automated, real-time reporting of scope 3 emissions in the construction sector.

Feedback, up 3.2%, announced that its AGM would be held at Temple Chambers, 3-7 Temple Avenue, London, EC4Y 0DT, on 26 October 2023 at 11:00 a.m.

Oracle Power, unchanged at 0.1p, in its interim results, announced that it reported nil revenues during the period. Loss before tax widened to £0.61m from £0.36m. As at 30 June 2023, cash balance stood at £0.33m (30 June 2022: £0.76m).

Cambridge Cognition, down 23.5%, in its interim results, announced that revenues rose to £6.04m from £5.88m recorded in the same period previous year. Loss before tax stood at £3.42m compared to a profit of £0.02m. Cash balance stood at £1.9m as at 30 June 2023 (31 December 2022: £8.3m).

IQGeo Group, down 11.0%, in its interim results, announced that revenues rose to £20.54m from £9.19m recorded in the corresponding period previous year. Loss before tax narrowed to £0.18m from £0.53m.

Frontier Developments, down 7.7%, announced that its Annual General Meeting (AGM) would be held on 01 November 2023 at The Trinity Centre, 24 Cambridge Science Park, Milton Road, Cambridge CB4 0FN.

Quartix Technologies, down 4.8%, announced that its Non-Executive Chairman, Paul Boughton has resigned from the company. Hence, the company’s founder Andy Walters has rejoined as Non-Executive Chairman.

Dialight, down 2.6%, announced that it has raised gross proceeds of up to £10.55m via the issue of 6,635,257 ordinary shares of 1.89p each by way of a placing to institutional investors and an offer to retail investors at a price of 159.00p per ordinary share.

Netcall, down 2.3%, announced that it would release its audited results for the year ended 30 June 2023 on 11 October 2023.

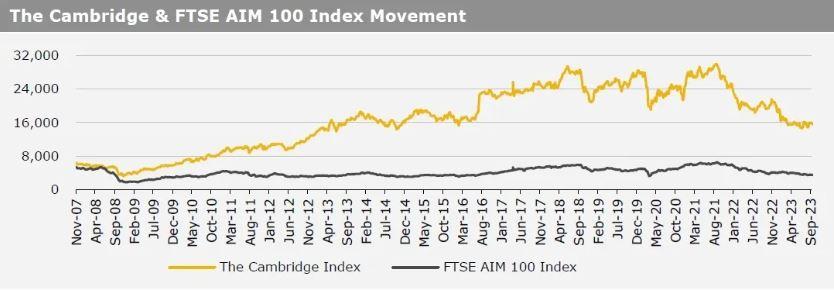

UK markets ended lower last week, amid fears that interest rates would remain higher for a longer period. On the macro front, UK’s current account deficit unexpectedly widened in 2Q23. On the flipside, Britain’s economy grew as anticipated in 2Q23, signalling a faster post-pandemic recovery, while the nation’s consumer credit accelerated in August. The FTSE 100 index declined 1.0% to settle at 7,608.1, while the FTSE AIM 100 index fell 1.9% to close at 3,452.6. Also, the FTSE techMARK 100 index lost 0.8% to end at 6,306.7.

US markets ended mixed in the previous week. On the data front, the US economy grew as expected in 2Q23, amid higher interest rates, while the nation’s initial jobless claims rose less than expected in the week ended 22 September 2023. Additionally, the US durable goods orders rebounded in August, driven by a rise in demand for machinery and other products, while the nation’s Richmond Fed manufacturing index improved in September. Meanwhile, the US consumer sentiment dropped to a four-month low in September, amid persistent concerns over high inflation and rising fears of a recession, while the Chicago Fed National Activity Index fell in August. Moreover, the US new home sales dropped in August while the nation’s pending home sales fell to its lowest level since April 2020 in August, due to higher mortgage rates. The DJIA index fell 1.3% to end at 33,507.5, while the NASDAQ index gained 0.1% to close at 13,219.3.