DS Smith, up 3.1%, announced the launch of its new Customer Innovation Hub in Madrid, Spain.

Johnson Matthey, down 1.3%, announced that it has opened its new offices in Riyadh, Kingdom of Saudi Arabia (KSA), extending its commitment to the region and aligning its strategic initiatives to enhance local support and collaboration within the region.

Hilton Food Group, up 1.0%, today, in its AGM trading update, announced that its trading performance has been in line with the Board's expectations, with volumes and sales ahead of the same period last year despite sales growth in some of the markets we operate being impacted by lower raw material prices. The group expects to publish its interim results for the 26 weeks ending 30 June 2024 on 04 September 2024.

SDI Group, up 22.3%, today, in its trading update for the year ended 30 April 2024, announced that it expects revenues to be in line with current market expectations at around £65.9m (FY23: £67.6m). Additionally, its adjusted operating profit is expected to be in the region of £9.6m (FY23: £12.8m) with adjusted profit before tax of approximately £8.0m (FY23: £11.8m), both in line with current market expectations.

IQGeo Group, up 16.5%, announced that it has agreed to be acquired by Geologist Bidco Limited (Bidco) for an enterprise value of £316m. Under the terms of the acquisition, IQGeo shareholders will be entitled to receive 480p in cash for each IQGeo share. It is intended that the acquisition will be effective through a court-sanctioned scheme of arrangement under Part 26 of the Companies Act. The scheme is expected to become effective in Q4 2024, subject to the satisfaction or, where permitted, waiver of the conditions.

Oracle Power, down 33.3%, along with its joint venture company, Oracle Energy Limited announced that they had received a no objection certificate (NOC) from the Sindh Environmental Protection Agency (SEPA) based on the Initial Environmental Examination (IEE) report, which is a part of the ESIA report. The NOC permits the construction of the proposed 1.3 GW renewable energy power plant in Jhimpir, Sindh Province, Pakistan. Separately, the company stated that its partner, Riversgold Ltd is set to commence a drilling program next week at the Northern Zone Gold Project in Western Australia. The operation aims to establish a maiden JORC-compliant gold resource, targeting a significant exploration goal of 2.5Moz to 4.8Moz of gold.

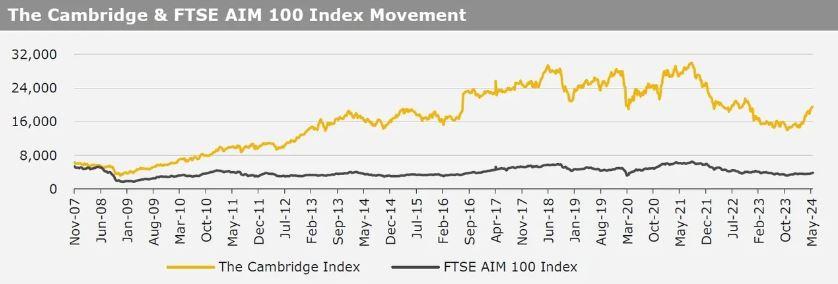

UK markets closed mostly lower last week. On the data front, the UK ILO unemployment rate rose as expected to three months in March. Meanwhile, the UK average earnings including bonus index advanced more than expected annually in the three months to March. The FTSE 100 index declined 0.2% to settle at 8,420.3, while the FTSE techMARK 100 index lost 1.1% to end at 6,926.6. Meanwhile, the FTSE AIM 100 index rose 0.6% to close at 3,842.6.

US markets ended higher in the previous week, following a slowdown in the US consumer price inflation boosted expectations for rate cuts by the US Federal Reserve (Fed). On the macro front, the US producer price index advanced as anticipated in April. Meanwhile, the US consumer price inflation slowed as expected in April, while the nation’s retail sales unexpectedly remained flat in April, indicating lower consumer spending. Additionally, the US housing starts advanced less than anticipated in April, while the nation’s building permits fell more than expected in April. Also, the US weekly jobless claims declined less than expected in the week ended 10 May 2024. Moreover, the US NY Empire State manufacturing index unexpectedly fell in May, while the nation’s Philadelphia Fed manufacturing index dropped more than expected in May. The DJIA index rose 1.2% to end at 40,003.6, while the NASDAQ index gained 2.1% to close at 16,686.