DS Smith, up 0.5%, announced that it has collaborated with Jonsac to boost the shift away from plastic packaging and towards sustainable paper alternatives within the European e-commerce market.

Johnson Matthey, down 0.1%, announced that it and BP's co-developed Fischer Tropsch (FT) CANS™ technology has been selected by DG Fuels for its first sustainable aviation fuel (SAF) plant in St. James Parish, Louisiana.

Darktrace, up 4.0%, in its trading update, announced that its revenue for the third quarter stood at $176.1m, indicating a yearly growth of 26.5%. Gross margin remained in the range as of 31 December 2023, while at 6.6%, One-year gross ARR churn remained equal to the range as of December 2023 and showed a 0.2 percentage point improvement in March 2023.

Oracle Power, up 50.0%, announced that it has entered into an exclusive option with Mining Equities to acquire the Blue Rock Valley Copper and Silver Project located in the Ashburton Basin in the northwest region of Western Australia. The project is located 165km southeast of Onslow, a multi-user port and the main port for the region's iron and LNG exports.

Bango, up 18.7%, in its full year results, announced that revenues rose to $46.09m from $28.49m recorded in the previous year. Loss before tax widened to $10.20m from $4.79m.

Checkit, unchanged at 21.0p, today, announced that it has introduced a new product, Asset Intelligence. This product module applies advanced analytics and Machine Learning to IoT data which will help enhance customer sustainability, reduce costs, and improve revenue.

CyanConnode Holdings, down 5.5%, today, announced that it has secured an order for 265,331 Omnimesh Modules from Madhyanchal One Infrastructure Private Limited, a subsidiary of IntelliSmart Infrastructure Private Limited (IntelliSmart). The supply of Omnimesh Modules for this project is expected to commence during Q1 FY 2025, and the supply of all hardware is expected to be completed during FY 2025.

1Spatial, down 0.9%, announced that it would release its audited final results for the year ended 31 January on 24 April 2024.

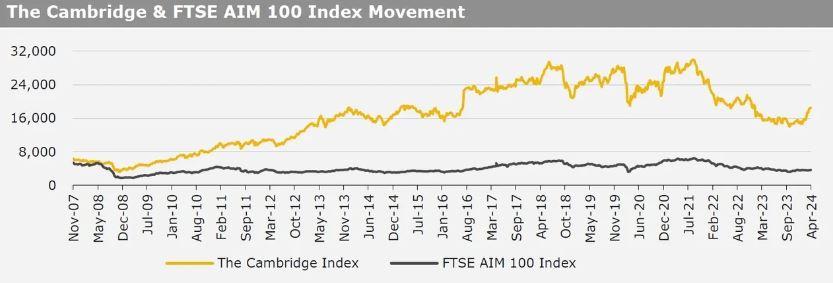

UK markets ended mostly higher last week, following upbeat Britain’s GDP data. On the data front, UK’s gross domestic product grew for the second month in February, indicating that the country would exit technical recession at the start of the year. Additionally, UK’s manufacturing production climbed more than anticipated in February, while the nation’s industrial production unexpectedly advanced in February. Moreover, UK’s BRC like-for-like retail sales rose more than expected in March, boosted by the Easter holidays, while the nation’s RICS housing price balance advanced more than expected in March. The FTSE 100 index advanced 1.1% to settle at 7,995.6, while the FTSE AIM 100 index rose 2.1% to close at 3,654.3. Meanwhile, the FTSE techMARK 100 index lost 1.5% to end at 6,696.6.

US markets ended lower in the previous week, amid rising geopolitical tensions in the Middle East and persistent worries over US inflation. On the macro front, the US producer price index advanced less than anticipated in March, while the nation’s Michigan consumer sentiment index dropped more than expected in April. Meanwhile, the US consumer price index rose more than expected in March, amid higher gasoline and shelter prices, while the nation’s weekly jobless claims dropped more than expected in the week ended 05 April 2024. Separately, the US FOMC minutes indicated that there is no rush to cut interest rates as inflation wasn’t moving lower quickly enough. However, the central bank still expects to cut interest rates later this year. The DJIA index fell 2.4% to end at 37,983.2, while the NASDAQ index lost 0.5% to close at 16,175.1.