DS Smith, down 3.1%, announced that it has chosen Amazon Web Services (AWS) as its preferred cloud provider to accelerate innovation, drive efficiencies, and support sustainable solutions.

Bango, up 8.7%, in its interim results, announced that revenues rose to $20.27m from $10.79m recorded in the same period previous year. Loss before tax widened to $4.94m from $1.21m.

IQGeo Group, up 3.2%, announced that it has secured a major new contract with top five global wholesale fibre network provider with operations across US and Europe having a software ACV value of $400,000 per annum and a total contract value over 3 years of $1.9m including ACV and services.

Dialight, down 26.9%, in its interim results for the period ended 30 June 2023, announced that revenues dropped to £73.20m from £80.80m recorded in the same period a year ago. Loss before tax stood at £4.20m compared to a profit of £1.60m. The company has not declared an interim dividend for 2023 (2022: nil). Separately, the company announced that its Chief Financial Officer and Executive Director, Clive Jennings has stepped down from her position, with immediate effect.

Xaar, down 7.0%, in its unaudited interim results for the six months ended 30 June 2023, announced that revenues fell to £34.52m from £36.61m recorded in the corresponding period previous year. Loss before tax widened to £1.82m from £0.30m. The company has declared no interim dividend for 2023.

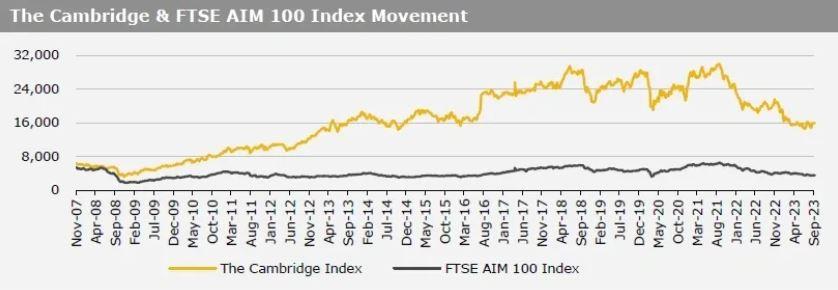

UK markets ended lower last week, on prospects interest rates will remain higher for longer. On the macro front, UK’s consumer price inflation unexpectedly slowed to an 18-month low in August, while the nation’s retail sales rose less than expected in August. Additionally, the UK public sector net borrowing posted a deficit in August, while the nation’s business activity shrank at its fastest pace in 32-months in September, stoking concerns over recession risk. Meanwhile, the GfK consumer confidence index unexpectedly advanced to its highest level since January 2022 in September. Further, the Bank of England, in its monetary policy meeting, kept its benchmark interest rates unchanged at 5.25%, for the first time since November 2021. However, the central bank signalled that rates would remain higher for longer to combat inflation. The FTSE 100 index declined 0.4% to settle at 7683.9, while the FTSE AIM 100 index fell 1.2% to close at 3517.9. Also, the FTSE techMARK 100 index lost 2.4% to end at 6357.1.

US markets ended weaker in the previous week, following Federal Reserve’s (Fed) hawkish remarks on interest rates. On the data front, the US housing starts fell to a 3-year low level in August, while the nation’s existing home sales dropped to a 7-month low in August, amid rise in mortgage rates. Additionally, the US Philadelphia Fed manufacturing index declined in September, while the nation’s services PMI fell in September. Meanwhile, the US building permits rose to its highest level since October 2022 in August, while the nation’s initial jobless claims dropped to an eight-month low in the week ended 15 September 2023. Separately, the OECD expects that the US economy to grow by 2.2% in 2023 and 1.3% in 2024. In the September meeting, the Fed kept its key interest rate unchanged at 5.50%, as widely expected. Moreover, the central bank indicated that it expects one more rate hike before the end of the year and reaffirmed that the interest rates are expected to be higher for a prolonged period. The DJIA index fell 1.9% to end at 33963.8, while the NASDAQ index lost 3.6% to close at 13211.8.